All Categories

Featured

Table of Contents

- – Why do I need Iul Cash Value?

- – What is the process for getting Indexed Univer...

- – Iul Premium Options

- – What is the process for getting Indexed Unive...

- – What is Indexed Universal Life Retirement Pl...

- – Who offers flexible Tax-advantaged Indexed U...

- – Who has the best customer service for Iul In...

In the occasion of a lapse, outstanding plan car loans in excess of unrecovered price basis will go through ordinary earnings tax. If a policy is a changed endowment contract (MEC), plan fundings and withdrawals will certainly be taxed as average revenue to the degree there are profits in the plan.

It's essential to keep in mind that with an exterior index, your policy does not straight get involved in any equity or set revenue investments you are not purchasing shares in an index. The indexes offered within the plan are constructed to maintain track of diverse sectors of the U.S

Why do I need Iul Cash Value?

An index may influence your interest credited, you can not get, directly participate in or receive reward payments from any of them through the policy Although an outside market index may affect your rate of interest attributed, your plan does not directly take part in any type of stock or equity or bond investments. IUL policyholders.

This content does not apply in the state of New York. Assurances are backed by the monetary stamina and claims-paying ability of Allianz Life insurance policy Business of North America. Products are issued by Allianz Life insurance policy Company of The United States And Canada, 5701 Golden Hills Drive, Minneapolis, MN 55416-1297. .

Shield your enjoyed ones and save for retired life at the very same time with Indexed Universal Life Insurance Policy. (Indexed Universal Life policy)

What is the process for getting Indexed Universal Life Vs Term Life?

HNW index global life insurance policy can aid collect cash money worth on a tax-deferred basis, which can be accessed throughout retired life to supplement earnings. (17%): Policyholders can typically borrow against the cash worth of their policy. This can be a resource of funds for different requirements, such as investing in a company or covering unanticipated expenditures.

(12%): In some cases, the money value and fatality benefit of these policies may be protected from financial institutions. Life insurance policy can likewise aid decrease the danger of an investment profile.

Iul Premium Options

(11%): These plans provide the possible to earn rate of interest linked to the performance of a securities market index, while additionally providing an ensured minimum return (IUL policyholders). This can be an eye-catching option for those looking for growth possibility with downside security. Resources forever Study 30th September 2024 IUL Survey 271 participants over 30 days Indexed Universal Life insurance policy (IUL) may seem complex initially, but understanding its auto mechanics is crucial to recognizing its complete possibility for your monetary preparation

If the index gains 11% and your involvement rate is 100%, your money value would be credited with 11% interest. It is very important to note that the maximum passion attributed in a provided year is capped. Allow's say your chosen index for your IUL policy got 6% from the beginning of June to the end of June.

The resulting interest is contributed to the cash value. Some plans compute the index gains as the sum of the changes for the period, while various other policies take approximately the everyday gains for a month. No rate of interest is attributed to the cash account if the index drops instead of up.

What is the process for getting Indexed Universal Life Loan Options?

The rate is established by the insurance provider and can be anywhere from 25% to even more than 100%. (The insurance provider can additionally alter the involvement price over the lifetime of the plan.) As an example, if the gain is 6%, the engagement rate is 50%, and the present cash value overall is $10,000, $300 is included in the cash worth (6% x 50% x $10,000 = $300). IUL policies commonly have a floor, typically evaluated 0%, which safeguards your money value from losses if the market index carries out adversely.

This offers a degree of safety and assurance for insurance holders. The interest attributed to your money value is based upon the performance of the chosen market index. Nevertheless, a cap (e.g., 10-12%) is normally on the maximum interest you can gain in a provided year. The part of the index's return attributed to your cash money worth is established by the participation price, which can vary and be readjusted by the insurance company.

Shop about and contrast quotes from various insurance policy companies to discover the most effective policy for your demands. Very carefully examine the plan illustrations and all conditions prior to choosing. IUL entails some level of market risk. Prior to picking this kind of policy, guarantee you fit with the potential fluctuations in your money worth.

What is Indexed Universal Life Retirement Planning?

By contrast, IUL's market-linked cash money worth growth provides the capacity for higher returns, especially in beneficial market conditions. Nevertheless, this capacity comes with the threat that the stock exchange performance might not provide regularly secure returns. IUL's adaptable costs settlements and flexible survivor benefit offer flexibility, interesting those looking for a plan that can evolve with their altering economic situations.

Indexed Universal Life Insurance Policy (IUL) and Term Life Insurance policy are different life plans. Term Life insurance policy covers a particular period, commonly in between 5 and half a century. It only gives a survivor benefit if the life guaranteed dies within that time. A term plan has no money worth, so it can't be used to offer life time advantages.

It appropriates for those seeking temporary defense to cover specific monetary commitments like a home loan or kids's education and learning fees or for organization cover like shareholder protection. Indexed Universal Life (IUL), on the various other hand, is an irreversible life insurance policy that offers protection for your entire life. It is much more costly than a Term Life policy due to the fact that it is created to last all your life and provide a guaranteed cash money payout on death.

Who offers flexible Tax-advantaged Indexed Universal Life plans?

Selecting the ideal Indexed Universal Life (IUL) plan has to do with discovering one that lines up with your economic objectives and run the risk of resistance. An experienced monetary advisor can be invaluable in this process, guiding you with the complexities and guaranteeing your selected plan is the ideal suitable for you. As you investigate acquiring an IUL plan, maintain these key considerations in mind: Understand just how attributed rates of interest are linked to market index efficiency.

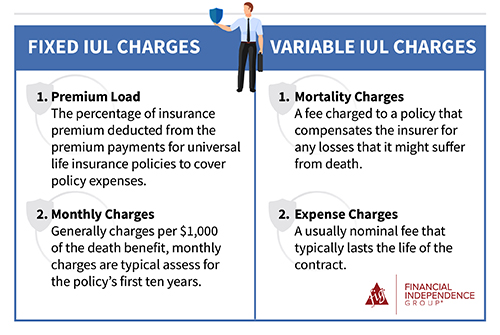

As outlined earlier, IUL plans have numerous fees. A greater rate can boost potential, yet when contrasting policies, assess the cash money value column, which will certainly help you see whether a greater cap rate is much better.

Who has the best customer service for Iul Insurance?

Different insurance companies supply variations of IUL. The indices linked to your plan will directly affect its performance. Versatility is crucial, and your policy ought to adapt.

{kind=link}

Table of Contents

- – Why do I need Iul Cash Value?

- – What is the process for getting Indexed Univer...

- – Iul Premium Options

- – What is the process for getting Indexed Unive...

- – What is Indexed Universal Life Retirement Pl...

- – Who offers flexible Tax-advantaged Indexed U...

- – Who has the best customer service for Iul In...

Latest Posts

Difference Between Whole Life Vs Universal Life

How Much Does Universal Life Insurance Cost

Level Premium Universal Life Insurance

More

Latest Posts

Difference Between Whole Life Vs Universal Life

How Much Does Universal Life Insurance Cost

Level Premium Universal Life Insurance